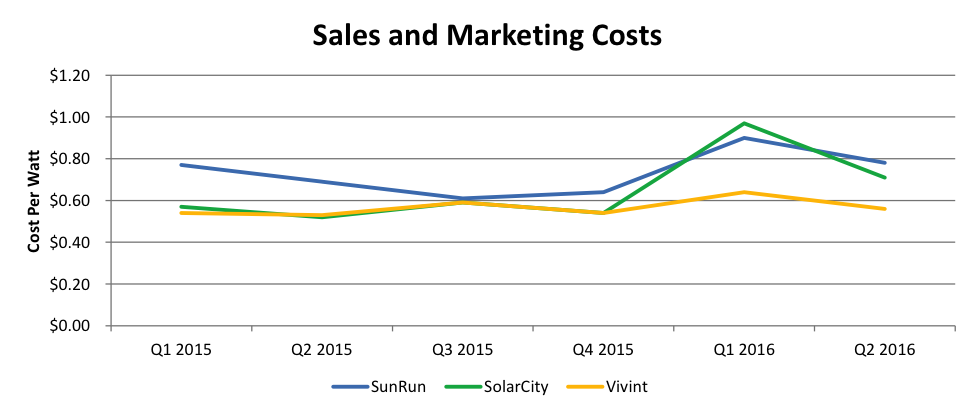

Increasing Solar Acquisition Costs

Residential solar acquisition costs have been increasing, partially driven by high levels of penetration in established markets of California, New York and Massachusetts. Our research indicates that several zip codes in California have exceeded 25% penetration (93314 in Bakersfield has reached 33.2%). A recent Reuters article covers this dynamic in Scripps Ranch, an affluent San Diego neighborhood. The large national installers reported a significant increase in acquisition costs in Q2 – an average increase across the three of 18.4% from the same period in the prior year. The national installers expect acquisition costs to decline in Q3 and have cited salesforce efficiency opportunities as the main driver and are also exploring new acquisition channels, including a recent partnership with SolarCity and AirbnB.

Web-based Solar Acquisition Platforms

Another development that will likely have a dramatic impact on residential solar acquisition costs and strategies is the increasing presence of web-based sales platforms, including EnergySage, PickMySolar, Sungevity, Powerscout, among others. Online solar platforms have grown to dominate more established international residential solar markets, including SolarQuotes and SolarChoice in Australia.

A recent report from EnergySage provides insight into how these web-based platforms are already having an impact on solar customer acquisition:

- Web-based platforms are being used to compare offers received from national installers. Over 30% of customers that joined EnergySage’s Marketplace had a solar quote already on hand, with 40%+ of those offers coming from a national installer. This comparison shopping behavior can be seen in the different levels of 3rd party ownership on the EnergySage Market place (96.3%) vs. nationwide (55.1%).

- 85% of consumers preferred a quote before a site-visit. Consumers’ preferences for quotes prior to a visit will likely impact the long-term success of canvassing techniques employed by national and local installers.

- Dizzying number of choices of solar panels and inverters. On the EnergySage platform, installers offered 46 brands of panels and 26 brands of inverters. 41% of solar installers offer 3 or more solar panel brands and 30% offer 3 or more inverter brands. Online platforms will help consumers navigate the increasing number of options.

Solar Acquisition Cost Outlook

Despite the recent increase in acquisition costs, an informative post from Sunrun CEO Lynch Jurich provides insight on why solar acquisition costs should decline in the long-term and why the current return on acquisition costs is comparable or even more attractive than those within other industries (wireless, retail electricity, and auto insurance).

Sunrun’s acquisition costs were ~$4,900 in Q2-16 ($4,667 in Q4-15) relative to a Customer Lifetime Value of ~$14,000 (calculated as $28,000 in Customer Contract Present Value less installation costs).

This compares favorably to other industries when you equalize the customer value as seen in the chart below. Sunrun also believes that this customer value is very certain due to the quality of the underlying contractors (1% loss rate in the last 10 years) and the positive dynamics of customer churn (they can contract again with SunRun and SunRun has retained 99% of value through churn events).

This compares favorably to other industries when you equalize the customer value as seen in the chart below. Sunrun also believes that this customer value is very certain due to the quality of the underlying contractors (1% loss rate in the last 10 years) and the positive dynamics of customer churn (they can contract again with SunRun and SunRun has retained 99% of value through churn events).

Sunrun also believes that these acquisition costs will come down overtime due to improvements in the customer experience from proposal to installation (permiting, audits, standardized procedures, etc.) and increased customer awareness as solar expands and gains relavance for national brands (retail electricity providers and membership associations) and a mature customer base generates low-cost referrals.

Sunrun also believes that these acquisition costs will come down overtime due to improvements in the customer experience from proposal to installation (permiting, audits, standardized procedures, etc.) and increased customer awareness as solar expands and gains relavance for national brands (retail electricity providers and membership associations) and a mature customer base generates low-cost referrals.

The analysis above that justifies the current level of spend in residential solar relative to other industries uses $14,000 of Customer Lifetime Value, but SunRun believes there are opportunities to increase this amount to close to $25,000 through contract extensions and expansion of other services including storage, home grid services and additional system capacity to support electric vehicle adoption.

Conclusion

The Sunrun analysis raises valid points on the rationality of current levels of acquisition spending and factors that could drive these costs down and the industry will look to Q3 earnings releases to see how successful installers were at managing their acquisition costs. The industry will also look to see how local installers perform vs. national installers, as recent data shows that national installer share has declined in certain markets, although this may have been due to a rationalization of acquisition spend this year. Although it is too early to draw conclusions, the increase usage of online web-based platform may drive prices down and level the playing field for national and local installers – EnergySage indicated that the median quotes on their platform in H1 2016 were $3.63 / watt vs. the national median of $4.39. This of course could decrease the Customer Lifetime Value used in the SunRun analysis.